A quick glance at the news would likely leave one strongly concerned, if not thoroughly convinced, of the inevitability of a global economic recession. As reported by the AP, “Kristalina Georgieva, managing director of the International Monetary Fund, told an audience at Georgetown University on Thursday that the IMF is once again lowering its projections for global economic growth in 2023, projecting world economic growth lower by $4 trillion through 2026.” Georgieva continued, saying “The risks of recession are rising,” and that “Things are more likely to get worse before [they] get better” in this “period of historic [economic] fragility”.

The IMF is not the only one sounding the alarm. Harvard professor of economics Ken Rogoff told Yahoo Finance that with regards to the US economy, “a really mild recession…would be lucky.” Former U.S. Treasury Secretary Larry Summers said in an interview on CNN that “it’s more likely than not” that the U.S. will enter a recession. Economic markets share their concerns– the stock market experienced precipitous drops on October 7, with the S&P closing 2.8% down, the Dow Jones Industrial Average 2.1% down, and the Nasdaq 3.8% down, largely due to recession fears, per the AP.

Not all major sources of economic authority are participants in such a doom-and-gloom narrative, however. Current U.S. Treasury Secretary Janet Yellen, a two-time former chairwoman of the Federal Reserve (a spot currently held by Jerome Powell), took care to avoid the word “recession” and defended the Fed’s rate hikes in remarks made this past Tuesday. “For major economies facing high inflation, the immediate task is to return to an environment of stable prices. Central banks bear the prime responsibility.”

But even Yellen acknowledged the growing fears of an economic downturn, saying “…it is important to recognize that macroeconomic tightening in advanced countries can have international spillovers.” Georgieva agreed, pointedly criticizing the Federal Reserve: “…tightening monetary policy too much and too fast – and doing so in a synchronized manner across countries – could push many economies into prolonged recession.”

Despite the heated debate over the level of risk, most experts agree that there is a tangible risk of an economic recession in the near future, with the immediate cause being the interest rate raises pursued by the Fed and other central banks. But why exactly is this the case, and what does all of this mean for the average consumer? In this column, I’ll give a lay-friendly explanation behind our potentially-impending economic crisis, with a particular focus on how we got to this point and how concerned one should be about the future of the economy.

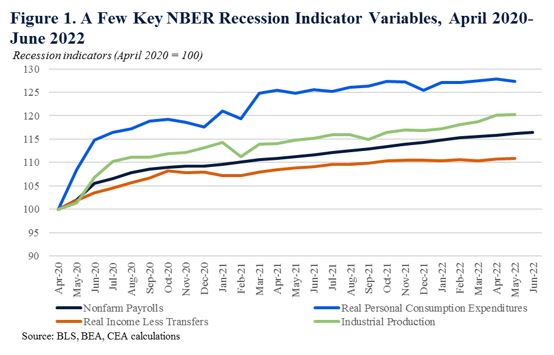

To begin with, it is important to understand the definition of an economic recession. The apocryphal rule of thumb has long been two consecutive quarters of falling real Gross Domestic Product (GDP, an aggregate of all the final goods and services produced within a country). The “official recession scorekeeper”, as described by the White House Council of Economic Advisers in a July 2022 press release, is the National Bureau of Economic Research (NBER), which defines a recession as “a significant decline in economic activity that is spread across the economy and that lasts more than a few months.” More specifically, the NBER measures recessions via various economic indicator indexes, which, if in decline over multiple months, lead the NBER to describe the economic environment as a recession. Shown in the graph below are what are generally believed to be the four biggest metrics: Nonfarm Payrolls, Real Income Less Transfers (or Real Personal Income), Real Personal Consumption Expenditures (or Real Retail Sales), and Industrial Production. The definitions of these are fairly self-explanatory, but a brief overview of each is still in order. Nonfarm payrolls measure the payroll of non-farm firms and are useful for assessing employment; consumption expenditures/retail sales measure how much the average consumer is spending, effectively measuring consumer demand; industrial production measures the output value of industries such as mining and energy; finally, real income measures how much the average household makes, adjusted for inflation. (Definitions courtesy of Advisor Perspectives). Now, for a look at the data:

While this data is somewhat dated (most recently updated June 2022), for there to be a recession by the NBER’s declaration, there would need to be a consistent, sustained decline in these indicators across the board as the White House somewhat gleefully notes in the explanation accompanying the graph. However, as a mere look at the graph indicates, growth has declined, which can be a precursor to a downturn.

Other economic indicators nevertheless give some reason for alarm. The U.S. Conference Board, a well-reputed independent economic research agency, found a decline in its Leading Economic Indicator (LEI) for the sixth straight month in August 2022 (September data is not available yet), leading the board to predict in its latest press release that “Economic activity will continue slowing more broadly throughout the US economy and is likely to contract…The Conference Board projects a recession in the coming quarters”.

The culprit mentioned for this slowdown in the Conference Board’s damning assessment? None other than the Fed: “A major driver of this slowdown has been the Federal Reserve’s rapid tightening of monetary policy to counter inflationary pressures.” Given the recurring mention of the Fed’s policy and its effects on the economy, the second component of understanding our risk for a recession is understanding the Fed’s actions – what they have done, why it matters, and what it means going forward.

The Fed, as it explains the matter itself, principally exerts its influence on the economy via altering the federal funds rate, commonly known as “raising or lowering interest rates.” Perhaps contrary to common misconception, the Fed does not directly establish these rates – instead, they affect them indirectly by altering the money supply available to banks for their reserves by buying or selling treasury bills from their primary dealers.

Deciphering the jargon, the Fed essentially aims to change the amount of money available to banks. When they have less money available, they charge higher interest rates, which discourages spending and encourages saving because people avoid borrowing money when the interest rate on said money is higher. When people borrow less money, they spend less; consumption decreases, demand decreases, and eventually, prices go down.

The final point is the most important there, as it answers the question of why the Fed has done what it has done. It most recently raised rates in September by 0.75 points – a large shift, by historical standards– bringing the total rate to 3.125%, a huge increase from the near-zero the rates sat at earlier this year. The why behind this move is prices, and in that vein, the i-word: inflation.

In August, the inflation rate sat at 8.3%, roughly meaning that goods and services are 8.3% more expensive now than they were this time last year. Inflation is dangerous and politically unpopular for obvious reasons: higher prices in necessities, such as gas, hit consumers’ wallets hard and fast. Inflation also decreases the value of the U.S. dollar and is generally bad for the economy at high rates (above 2-4%).

Exploring inflation, including its causes and consequences, would take an entirely separate piece, so I’ll stick to the bare minimum. Essentially, inflation results from an oversupply of money in the market, which can be caused by government spending, supply chain shortages, an increase in the cost of the factors of production, etc. In order to combat it, the Fed raises rates in an effort to decrease spending, and contract the quantity of money in the economy.

Here is where things become far more intuitive. With less spending, businesses earn less money. To avoid going underwater, they stop hiring new employees, slash wages, and eventually lay off workers. That causes rises in unemployment, lower household incomes, lack of ability to pay rent, buy necessities…in short, all the worst symptoms associated with a recession. Hence, while lowering inflation to make life affordable is paramount, taking stringent measures to do so can effectively backfire.

Now, at long last, I can address the question at hand: are we staring down a global recession? The unfortunate answer is that I can’t really declare anything for certain, but I am inclined to say yes. As Nobel laureate Paul Krugman notes in The New York Times, “…all of this [effort to combat inflation] takes a while…current inflation and employment are basically telling us about the past; we need to look to other data for a glimpse of the future.” While current economic numbers remain fairly robust, future indicators are far less so.

Still, the Fed remains undaunted in its raising rates, which seems likely to have unwanted effects down the line. Lower prices come at the cost of a tighter job market, more expensive housing, and lower wages. Furthermore, prices on key goods such as fuel, technology, fabric, and grain may remain entrenched due to supply chain shortages caused by Russia’s war with Ukraine and China’s continuation of its zero-COVID policy. That, in turn, may cause the Fed to pursue even greater constrictive monetary policy, thereby exacerbating matters.

The future is uncertain, and we may yet dodge a recession. But unfortunately, conventional wisdom does not give much reason for hope on that front.