Image via Institute for New Economic Thinking

***

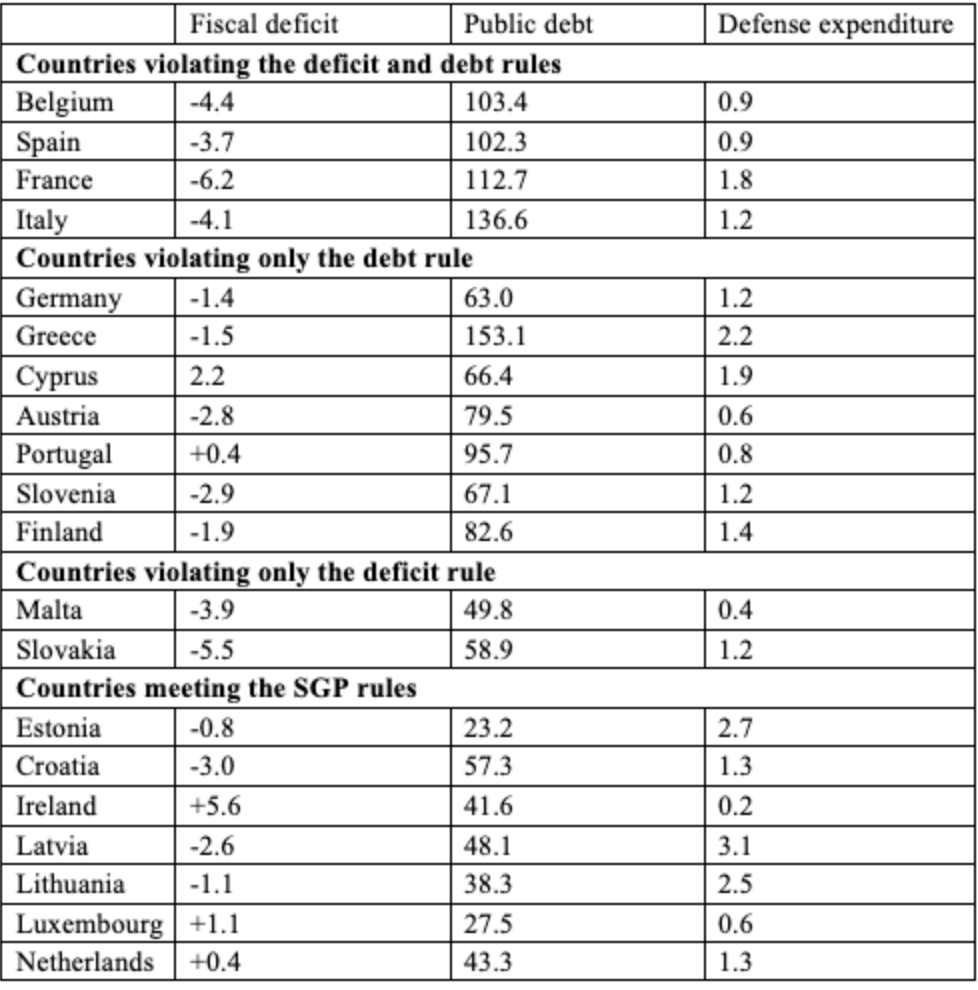

Times are desperate. The 2024 European balance sheet suggests a rather dire situation, with twelve Eurozone countries carrying public debt above the Stability and Growth Pact’s 60 percent of GDP ceiling. Five—Belgium, France, Greece, Italy, and Spain—exceed 100 percent. Italy’s debt stands at roughly 140 percent of GDP; Greece remains above 160 percent despite years of consolidation. Even Germany, long the emblem of fiscal rectitude, sits above the formal threshold at approximately 63 percent.

The fiscal situation in the Eurozone countries, 2024, Image via the European Commission

***

Growth has also been anemic. The post-pandemic rebound faded quickly, weighed down by the energy shock following Russia’s invasion of Ukraine and tighter monetary policy from the European Central Bank. Between the fourth quarter of 2019 and the fourth quarter of 2023, the Euro-area economy grew by around 3% in cumulative terms, while real GDP in the United States rose by more than 8%. Germany, the continent’s industrial engine, has flirted with recession, burdened by weak export demand and high energy costs. Italy’s long-term growth rate remains chronically low, constrained by productivity stagnation and demographic decline. Therefore, amid economic crises and war on the continent, European leaders return again and again to one prescription: austerity.

Indeed, Europe has a tradition of austerity. The Stability and Growth Pact institutionalised austerity in the Eurozone’s architecture. Limiting deficits to 3 percent of GDP and public debt to 60 percent of GDP, the one-size-fits-all approach has acquired quasi-moral status. Germany, for instance, with the so-called “debt brake” (Schuldenbremse) embedded in the Basic Law (Grundgesetz) limits federal structural borrowing to 0.35 percent of GDP per year. Austerity is depoliticised, seen as the virtuous, responsible policy to implement. Indeed, the debate quickly slides into a moralizing discussion where supporters see it as a virtuous self-denial while critics claim it as counter-productive nonsense.

The intellectual case for austerity is simple: governments, like households, cannot spend beyond their means indefinitely. Rising debt increases borrowing costs, undermines investor confidence, and risks fiscal crisis. If deficits grow unchecked, markets may impose discipline brutally and do so suddenly.

Therefore the data regarding austerity, like in all social sciences, is complicated. As George Box, British statistician, points out “all models are wrong but some are useful.” Regarding austerity, research conducted by Now Ropes professor of political economy, Alberto Alesina, and Carlo Favero and Francesco Giavazzi of Bocconi University in their book When It Works and When It Doesn’t, suggests that austerity achieved primarily through tax increases tends to trigger recessions and can even worsen a country’s debt load by shrinking GDP. By contrast, consolidation through targeted spending cuts appears to have a smaller negative impact on output, though the social consequences can be severe. Even this apparent clarity dissolves under scrutiny. Outcomes depend on the economic cycle, interest rates, exchange-rate regimes, and external demand. A country that tightens fiscal policy during a deep recession may entrench stagnation. A country that consolidates during a robust expansion may dampen overheating without major harm. But there are no randomized trials for nations. Each economic outcome is entangled with politics, institutions, and global conditions.

Furthermore, Europe’s great austerity experiment has failed on its own terms during the Euro-crisis. While the United States pursued fiscal stimulus and returned relatively quickly to sustained growth, several European countries that adopted front-loaded spending cuts and tax increases, such as Greece, Spain, Portugal, and the UK, experienced prolonged stagnation, soaring unemployment, and in some cases rising debt-to-GDP ratios as shrinking output offset deficit reduction. In Greece, GDP fell by more than 25 percent, and debt burdens worsened despite severe consolidation. Research shows that the composition and timing of austerity matter, but the broader pattern indicates that synchronized tightening across fragile economies lacking monetary flexibility can entrench downturns rather than restore confidence. At the same time, cuts to social protection coincided with measurable social costs, including rising suicide rates in the hardest-hit countries, reinforcing the argument that austerity has often been not only economically counterproductive but also socially damaging.

The lesson is not that fiscal discipline is irrelevant. In the long term, unsustainable debt constrains sovereignty and policy choice. But the European experience suggests that timing, composition, and institutional context are decisive. Austerity imposed in a slump, across multiple interconnected economies, without offsetting monetary or fiscal expansion elsewhere, risks becoming procyclical, deepening the very crisis it aims to solve.

So what are the alternatives? Europe is still in debt. France has lost its financial credibility, and is now cutting in education, culture and benefits. Italy is still struggling with healthcare as austerity measures have increased general mortality, suicide rates and fatalities from cancer and heart disease. The rearmament efforts also garner a significant cost. The money needs to come from somewhere.

For alternatives to austerity, France will be considered as a case study. In France, the core problem is not a lack of resources but the misalignment of priorities and rigid structures that prevent efficient allocation of funds. Rather than cutting public services to meet deficit targets, policymakers could reallocate resources, modernize labor laws, and invest strategically to stimulate the economy.

At the European level, coordinated fiscal tools could also relieve the pressure on individual states. Joint borrowing and EU-wide investment programs could fund growth-promoting projects, spread risk, and allow France to invest in health, education, and green energy while stabilizing its finances. Economists stress that timing and composition matter: austerity during downturns often deepens stagnation, whereas well-targeted investments in periods of slow growth can generate higher GDP and, ultimately, improve debt sustainability.

Another solution comes back to the good old Tax The Rich tale. Indeed, the “Zucman tax” was brought before Parliament and would have imposed a 2 % levy on net assets above €100 million, potentially raising €15-20 billion annually to help address the country’s budget deficit. Although it passed the lower house at one point, the measure was ultimately rejected by the Senate amid concerns about investment, capital flight, and constitutional challenges.

Another measure could be restructuring France’s cumbersome administration and bureaucracy, which costs the country around €84 billion as estimated by the French think tank, IFRAP. Roughly a quarter of the workforce is in public service, and public spending consumes 56% of GDP, yet overlapping responsibilities, excessive regulations, and a culture of centralization have created a rigid, costly, and opaque system. Bureaucracy grows through self-interest, political collusion, and cronyism, while decentralization efforts often expand, rather than reduce, administrative layers. Fewer layers of administration would speed decision-making, reduce delays caused by excessive regulations, and lower the costs of implementing public services. Instead, in the new budget, France will be laying off 4,000 teachers while creating 8,000 bureaucrats.

Belt tightening continues to be politically preached as the only policy to save bankruptcy, while governments fail to tackle deep-seated, systemic inefficiencies. Why? Because cutting spending is easy. As long as austerity is seen as the morally responsible response to fiscal deficits, meaningful administrative and structural reforms can be conveniently overlooked, ensuring the working class carries the burden of economic mismanagement, draining the very resources the state needs to repay its debts.

***

This article was edited by Siera Calderon.